Table of Contents

If you cause a car crash in Denver, who pays for the other driver's injuries? That’s where bodily injury liability (BIL) coverage comes in. As a cornerstone of your auto insurance, this coverage acts as your primary financial shield, covering the other party's medical bills, lost wages, and pain and suffering up to your policy limits.

Understanding what is bodily injury liability coverage is not just an insurance technicality—it’s a critical part of protecting your financial future. At Conduit Law, our Denver personal injury team has recovered over $50 million for clients, and we've seen firsthand how the right coverage can prevent a car accident from turning into a financial catastrophe. This guide breaks down exactly what this coverage does and why Colorado's minimum requirements are a dangerous gamble.

Your Financial Shield in an At-Fault Accident

Getting behind the wheel in Denver comes with a heavy dose of responsibility. Colorado operates under a "tort" or at-fault insurance system. In plain English, if you cause a wreck, you’re legally and financially on the hook for the damage and injuries you cause.

This is exactly why bodily injury liability coverage is one of the most critical pieces of your auto policy. Without it, you’d be forced to pay for someone else’s medical treatments, rehab costs, and lost income directly out of your own pocket.

A serious collision on I-70 or even a fender-bender on Colfax Avenue could quickly spiral into a financial catastrophe, putting your home, savings, and future earnings at risk.

Protecting Your Personal Assets

Let's make this real. Imagine you cause an accident that leaves the other driver needing surgery and months of grueling physical therapy. Their medical bills could easily soar past $100,000, and that’s not even counting the paychecks they lose while out of work.

If you only carry Colorado's legally required minimum coverage, you are personally responsible for every dollar that exceeds your policy limits.

Your bodily injury liability coverage is designed to step in and handle these massive costs. It acts as a crucial buffer between an awful day on the road and your long-term financial stability, ensuring the injured person gets the compensation they need without bankrupting you in the process.

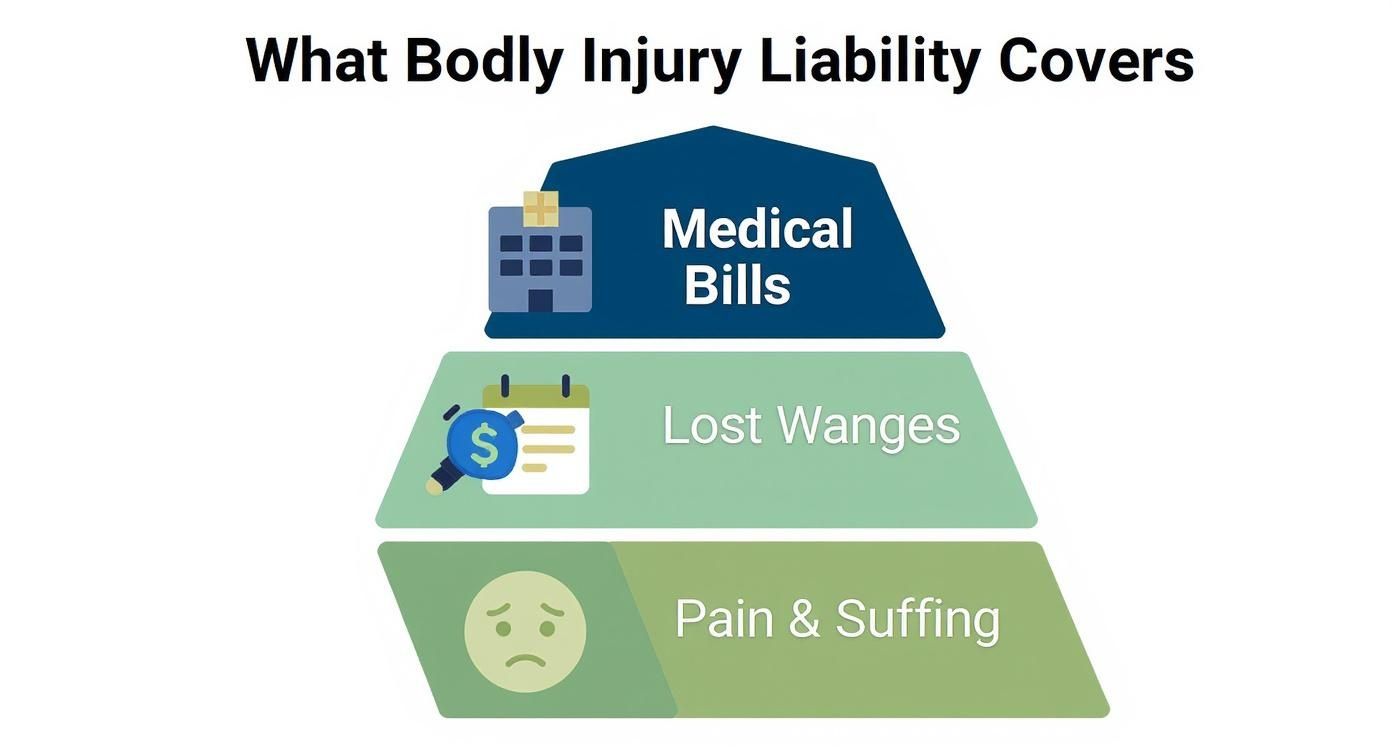

Bodily injury liability coverage is not for your injuries; it is exclusively for the injuries you cause to others. This is one of the most fundamental concepts in understanding how auto insurance really works in Colorado.

To break it down even further, here’s a quick-glance table showing what this essential coverage handles versus what it doesn't.

Bodily Injury Liability At a Glance

| Coverage Aspect | What It Covers (For the Other Party) | What It Does NOT Cover |

|---|---|---|

| Medical Expenses | ER visits, surgery, hospital stays, physical therapy, and future medical care related to the accident. | Your own medical bills (that’s for your health insurance or MedPay coverage). |

| Lost Wages | Income the injured person loses because they are unable to work while recovering. | Your own lost wages if you are injured. |

| Pain & Suffering | Compensation for physical pain, emotional distress, and loss of enjoyment of life resulting from their injuries. | Your own pain and suffering. |

| Legal Fees | Your legal defense costs if the injured party sues you over the accident. | The other party’s attorney fees (this is paid from their settlement). |

| Property Damage | Nothing. This does not cover damage to the other person's car or property. | Damage to the other driver's vehicle (that's for Property Damage Liability). |

This table provides an immediate, clear understanding of what BIL is for. It's all about paying for the human cost of an accident you cause, not the property damage or your own injuries.

Why Every Denver Driver Needs This Coverage

This coverage isn't just a smart idea—it's the law. The state of Colorado mandates that every driver carry a minimum amount of BIL insurance to operate a vehicle legally. The problem? As we’ll explore later, the legal minimum often falls dangerously short of covering the actual costs of even a moderate accident.

At Conduit Law, we've seen firsthand how adequate liability coverage is the difference between a manageable situation and a life-altering financial disaster. Understanding what this policy covers and why it matters is the first step toward responsible driving and securing your financial future. It’s the core protection that allows our at-fault system to work, providing a clear path for victims to get compensated while shielding responsible drivers from devastating personal liability.

What Bodily Injury Liability Actually Pays For

When you hear “bodily injury liability,” most people think of the ambulance ride and the emergency room bill after a crash. That’s definitely part of it, but it’s just the tip of the iceberg. This coverage is designed to handle a much wider range of costs that pop up when someone gets hurt because of something you did behind the wheel.

Think of it as your financial shield. It’s there to pay for the other person’s damages, not your own. It’s meant to cover the immediate, short-term, and long-term consequences of an accident, making the injured person financially whole again. The costs can be absolutely staggering—far more than most people could ever afford to pay out of their own pocket.

Immediate Medical Expenses

The first wave of bills after a collision is usually for immediate medical care. These are the most urgent costs, and they can pile up incredibly fast.

- Emergency Services: This covers the ambulance that picks someone up from the scene. Just that ride alone can run into thousands of dollars here in the Denver metro area.

- Hospital Care: This is the big one. It pays for ER treatment, X-rays, CT scans, and any surgeries needed right away.

- Initial Doctor Visits: It also includes follow-up appointments with specialists to figure out the full extent of the injuries and get a treatment plan started.

These initial costs can blow past Colorado’s minimum coverage limits in a heartbeat. A single night in the hospital can easily generate bills that far exceed the state-mandated $25,000 per-person minimum, which is a scary thought if you’re underinsured.

Long-Term Recovery and Rehabilitation Costs

Many injuries from car accidents don't just heal in a week. They often require months, or even years, of ongoing care. Bodily injury liability is structured to cover these long-term costs, which are absolutely essential for a victim’s recovery.

This category often makes up the biggest chunk of a claim. It can include:

- Physical Therapy: Many people need extensive physical therapy to get their mobility and strength back.

- Rehabilitation Services: For severe injuries like a traumatic brain injury (TBI) or spinal cord damage, this might involve specialized inpatient rehab programs.

- Ongoing Medical Treatment: Think follow-up surgeries, pain management appointments, and prescription medications needed for the long haul.

- Medical Equipment: This covers the cost of things like wheelchairs, crutches, or even modifications to a person's home to accommodate a new disability.

Without proper coverage, an at-fault driver could be facing financial ruin, while the victim is left with a mountain of medical debt and an incomplete recovery.

Non-Medical Financial Losses

Bodily injury liability isn't just about paying medical bills. It’s also there to compensate the injured person for the very real financial hits they take when they can't work or live their life the way they used to.

At its core, this coverage is about restoring the victim's financial stability. It recognizes that an injury's impact goes beyond the physical, affecting a person's ability to earn a living and maintain their quality of life.

Here are the key non-medical costs it covers:

- Lost Wages: If the injured person is out of work while they recover, this coverage pays them for the income they’re missing. This is what helps families pay the mortgage and keep the lights on when a primary earner is laid up.

- Loss of Future Earning Capacity: In tragic cases where someone is permanently disabled and can no longer do their job, the policy can pay for the wages they would have earned over the rest of their career.

These financial stakes are incredibly high. Bodily injury liability is often bundled with property damage in policies with "split limits," which you'll see written as three numbers like 25/50/20. Those numbers are the absolute maximum your insurer will pay. If the damages are higher than your policy limits, you’re personally on the hook for the rest. For a deeper dive into these policy structures, you can learn more about how bodily injury liability policies work.

Compensation for Pain and Suffering

This is probably the most misunderstood part of a claim. Bodily injury liability also covers pain and suffering. This isn’t about a specific bill; it’s non-economic compensation that tries to put a dollar value on the human cost of the injury. It’s for the physical pain, the emotional distress, and the simple loss of being able to enjoy life.

Figuring out this amount is incredibly complex, which is why having an experienced personal injury attorney in your corner is so critical. An insurance adjuster will almost always try to downplay these damages, but they are a real and significant part of any serious injury claim. At Conduit Law, our experience ensures these intangible losses are properly valued and aggressively fought for.

Decoding Your Policy Limits: Per Person vs. Per Accident

When you glance at your car insurance policy, you’ll probably see a pair of numbers like 50/100 or 100/300. These aren't just industry jargon; they are the absolute heart of your bodily injury liability coverage. They represent the maximum amount of money your insurance company will pay if you cause an accident that hurts someone else.

Getting a handle on what these numbers mean is one of the most important things you can do to protect your financial future.

These numbers are your policy limits, and they’re split into two critical parts.

The Per-Person Limit

The first number in the pair (the "100" in a 100/300 policy) is your per-person limit. This is the absolute ceiling on what your insurer will pay out for the injuries sustained by any one single person you injure in a crash where you are at fault.

Let's say you have a $100,000 per-person limit. If you cause an accident that leaves another driver with $150,000 in medical bills, lost income, and other damages, your insurance will pay the first $100,000. That leaves you on the hook for the remaining $50,000. Creditors can come after your personal assets—your savings, your investments, even your home—to cover that debt.

This is exactly what that per-person limit is meant to cover.

As the infographic shows, these three categories of damages can skyrocket in a hurry, which is why a single person's claim can blow past a lower policy limit without much trouble.

The Per-Accident Limit

The second number (the "300" in a 100/300 policy) is the per-accident limit. This is the total maximum amount your insurance will pay for injuries to everyone combined in a single accident you cause. It doesn't matter how many people get hurt.

Think of it as the ultimate cap for that one incident. Even with a $100,000 per-person limit, your policy will not pay a dime over the $300,000 per-accident total for that single event.

Key Takeaway: The per-accident limit is the hard ceiling for a single crash. Whether two people are injured or five, your insurer's total payout for bodily injury will never go beyond this number.

A Real-World Denver Scenario

Picture this: you’re heading down I-25 during rush hour. You look away for just a second and end up causing a three-car pileup.

- Driver A has serious injuries totaling $120,000.

- Driver B has moderate injuries adding up to $80,000.

- A passenger in Car C has injuries that total $70,000.

The grand total for all injuries is $270,000. If you have a 100/300 policy, here's how things shake out.

Your $100,000 per-person limit isn't enough to cover Driver A's full $120,000 claim. That means you are now personally on the hook for the $20,000 difference. Meanwhile, the claims for Driver B and the passenger fall comfortably within your limits.

This example cuts to the core of why this coverage exists: it’s there to financially protect you when you cause an accident that injures other people. A widely recommended policy in the U.S. is 100/300, which gives you up to $100,000 for one person and $300,000 total for everyone in a single crash. To learn more about how these policies are set up, you can explore more about bodily injury liability insurance.

Picking the right limits is always a balancing act between what you can afford and what you need for real protection. Colorado's legal minimums are dangerously low, and one bad accident can easily leave you exposed. At Conduit Law, we've seen far too many cases where cheap, inadequate coverage turned a car crash into a full-blown financial catastrophe. A quick chat with an attorney can help you see the risks clearly and make sure you have the right protection in place before you ever need it.

Why Colorado's Minimum Coverage Is a Financial Gamble

It's easy to assume that if you have the minimum insurance Colorado requires, you're "covered." But in reality, just meeting the state-mandated minimums is one of the biggest financial risks you can take as a driver.

The law says you need at least $25,000 in bodily injury coverage per person and $50,000 per accident. On paper, that might seem like a lot of money. But when you see what a serious injury actually costs, you realize how dangerously inadequate those numbers are.

Think of it this way: the state minimum is the legal floor, not a financial safety net. It’s just enough to let you drive legally, not enough to protect you from financial ruin after a bad wreck.

The Massive Gap Between Law and Reality

The true cost of a car accident injury can be absolutely staggering. A single trip to the ER after a crash—with an ambulance ride, an MRI, and a few follow-up visits—can easily blow past the $25,000 per-person limit.

If the injuries are more severe and require surgery, a hospital stay, or long-term physical therapy, the costs will skyrocket.

Let’s look at some real-world numbers for common medical expenses after a crash:

- Ambulance Transport: It’s not uncommon for this to run over $2,000 right here in the Denver metro area.

- Emergency Room Visit: A serious visit involving imaging and tests can easily hit $5,000 to $15,000.

- Orthopedic Surgery: Fixing something like a broken leg often costs $30,000 to $50,000 or more.

- Traumatic Brain Injury (TBI) Treatment: Costs here can spiral into the six figures, often requiring years of rehabilitation.

Once you add lost wages and pain and suffering on top of these medical bills, it becomes painfully clear that $25,000/$50,000 offers a false sense of security. It's not a shield; it’s more like a paper umbrella in a hailstorm.

A Tale of Two Financial Futures

Picture this: you cause an accident on Speer Boulevard, and the other driver ends up with a broken femur that needs surgery. After everything is said and done, their total damages—including medical bills, physical therapy, and lost paychecks—add up to $75,000. Your insurance policy has the Colorado minimum, so it pays out its limit of $25,000.

This leaves a $50,000 shortfall. This isn't a bill the insurance company handles; it's now your personal debt. The injured party’s attorney can pursue your assets—your savings, your investments, and even place a lien on your home—to collect that remaining balance.

This is a scenario we at Conduit Law see all too often. A driver thought they were doing the right thing by having insurance, only to discover their low-cost policy has just triggered a life-altering financial crisis.

Across the United States, legislative priorities have shaped varying minimum insurance requirements. While several states mandate a baseline of $25,000 per person and $50,000 per accident, the actual costs from injury crashes frequently exceed these amounts. Medical expenses from serious accidents can climb over $100,000, highlighting how legally mandated limits often fail to protect drivers from financial ruin. If you'd like to understand more about these requirements, discover more insights about bodily injury liability insurance on dat.com.

Buying coverage well above the state minimum isn't about being upsold; it's about self-preservation. It’s the single best thing you can do to protect your family’s financial future from the devastating fallout of one bad day on the road. For a deeper dive into what the law requires, you can learn more about Colorado auto insurance requirements in our dedicated article.

How to File a Claim Against the At-Fault Driver

When another driver's mistake leaves you hurt, their bodily injury liability insurance is the policy that's supposed to cover your damages. The problem is, getting that compensation means going through a claims process designed to protect the insurance company’s profits, not your well-being. Knowing the right moves to make—and the traps to sidestep—is everything.

The entire process kicks off the second the crash happens. Your first priority is always your safety and getting medical care, but what you do at the scene can make or break your claim down the road.

What to Do Right at the Accident Scene

The moments after a collision are pure chaos, but a few clear-headed actions can lay the foundation for a successful claim. If you're physically up to it, switch into information-gathering mode.

- Call 911. Always. Get police and paramedics on the way. A police report creates an official, unbiased record of the incident, which is worth its weight in gold.

- Swap Information. You need the other driver's name, address, phone number, driver's license number, and, most importantly, their insurance company and policy number.

- Document Everything. Your phone is your best tool. Take pictures of both cars from every angle, the wider accident scene, any injuries you can see, and even things like skid marks or relevant traffic signs.

- Find Witnesses. If anyone saw what happened, get their name and phone number. An independent witness can be a powerful voice confirming your side of the story.

This is critical: do not admit fault or even apologize. An innocent "I'm so sorry" can be twisted by an insurer to mean you're accepting blame for the crash. Stick to the facts, and only the facts, when you talk to anyone, including the police.

Putting the At-Fault Driver's Insurer on Notice

Once you have the other driver’s insurance details, you have to formally open a claim with their company. This is what's known as a "third-party claim" because you’re not their customer—you’re a claimant. You can usually start the process online or by calling the claims number on their insurance card.

When you make that first call, be ready with the basics: date, time, location, and a short, factual account of what happened. The insurance company will assign a claims adjuster to your case. It’s vital to understand that this person's job is to investigate your claim and resolve it for as little money as possible.

From your very first conversation, remember the adjuster for the at-fault driver is not your friend. Their goal is to protect their company's bottom line. Be polite, but always be on guard.

The Adjuster's Investigation and Their Playbook

The adjuster will kick off an investigation to figure out who was at fault and how much your damages are worth. This is where you have to be the most careful. Adjusters are trained negotiators who rely on a standard playbook of tactics to minimize what they have to pay you.

- The Recorded Statement Trap: They will almost certainly ask for a recorded statement. You are not required to give them one, and it is almost never a good idea. They are pros at asking questions designed to trip you up, and they will use your own words against you to deny or devalue your claim.

- The Quick Settlement Ploy: Don't be surprised if you get a settlement offer just a few days after the crash. This is a huge red flag. It’s a lowball offer meant to close out your case before you even know the full extent of your injuries or what future medical care you might need.

- The Overly Broad Medical Release: The adjuster will send you a medical authorization form to sign. Be extremely careful. Signing a blanket release gives them the keys to your entire medical history, which they will dig through to find any pre-existing condition they can use to argue your injuries weren't caused by the crash.

Insurance companies have a whole host of reasons they use to justify underpaying or denying perfectly valid claims. To get a better sense of their motivations and tactics, you can read our guide explaining why insurance companies deny claims and what you can do about it.

Trying to handle this process on your own puts you at a massive disadvantage. When you have an experienced personal injury attorney from Conduit Law in your corner, you have a professional managing these communications, shielding you from these tactics, and fighting to get you the full compensation you deserve.

Why a Denver Attorney Is Your Strongest Ally

Filing a claim against an at-fault driver’s insurance seems like it should be straightforward. In reality, it’s a process loaded with traps for the unwary. You’re not dealing with a helpful service—you’re up against a massive insurance company whose entire business model is built on protecting its profits. And that means paying you as little as possible.

Going it alone puts you face-to-face with trained adjusters who use specific, well-practiced tactics to devalue your claim from the very first phone call. This is where partnering with an experienced attorney from Conduit Law flips the script entirely, shifting the power dynamic back where it belongs: with you.

Maximizing Your Financial Recovery

The single biggest value a lawyer brings to the table is the ability to calculate the full scope of your damages. An adjuster might throw out a quick settlement offer that covers your immediate emergency room bills. But what about the surgery you’ll need next year? The months of physical therapy? The wages you'll lose while you’re out of work recovering?

We look at the whole picture, especially the non-economic damages that insurers love to downplay or ignore completely.

- Future Medical Needs: We don't just look at past bills. We consult with medical experts to project the costs of the long-term care you're going to require down the road.

- Lost Earning Capacity: If your injuries permanently impact your ability to do your job, we calculate the total value of that loss over the course of your working life.

- Pain and Suffering: We build a powerful, evidence-backed case to demand fair compensation for the physical pain and emotional trauma you’ve been forced to endure.

An unrepresented person is completely at the mercy of the insurance company's valuation. With a lawyer, you have a professional advocate building a data-backed demand package designed to secure every dollar the law allows.

A Case Study in Advocacy

Consider a client of ours who was rear-ended on I-225 and suffered a serious neck injury. The at-fault driver’s insurance company initially offered $18,000, calling it a “generous” offer that would cover his ER visit. What they conveniently ignored was the complex spinal fusion surgery his own doctor said he needed.

He felt pressured, confused, and completely overwhelmed. The moment he hired Conduit Law, we took over all communication with the insurer. We gathered every medical record, got expert opinions on his future medical costs, and calculated his total projected damages—including lost income and pain and suffering—at over $250,000.

Faced with our comprehensive demand and the very real threat of a lawsuit, the insurer’s attitude changed completely. We ultimately secured a settlement that not only covered his surgery but also gave his family the financial stability they desperately needed. This is the difference an advocate makes.

To learn more about how we fight for our clients, see how a Denver personal injury lawyer can protect your rights.

Your Top Questions About Bodily Injury Liability, Answered

Even after breaking it all down, it's completely normal to have a few lingering questions. Bodily injury liability is a complex piece of the insurance puzzle, and the stakes couldn't be higher when you need it. Here are some straight answers to the questions we hear most often from Colorado drivers.

Does My Own Bodily Injury Liability Cover My Injuries?

No, and this is probably the single most important thing to get straight. Your bodily injury liability coverage is designed to pay for injuries to other people when you're the one legally at fault for the crash. It's there to protect your assets from a lawsuit.

So, how do you cover your own medical bills? You'll rely on a few other pieces of your financial safety net:

- Your Health Insurance: This should always be your first line of defense for your own medical care after an accident.

- Medical Payments (MedPay) Coverage: This is an optional but incredibly useful part of your auto policy. MedPay covers medical costs for you and your passengers, no matter who was at fault.

- The At-Fault Driver's Policy: If the other driver caused the wreck, our firm would pursue a claim against their bodily injury liability policy to pay for your damages.

What Happens If the At-Fault Driver's Coverage Isn't Enough for My Bills?

This is a scary situation, and unfortunately, it happens all the time. When the at-fault driver's policy limits are too low to cover the full extent of your damages, your own Underinsured Motorist (UIM) coverage is designed to kick in and make up the difference.

UIM coverage is there specifically for this gap. It bridges the distance between your total medical bills, lost wages, and other damages, and the other driver's cheap, inadequate policy.

Without it, your only other option is often to sue the at-fault driver personally for the remaining amount. That's a long, draining process with no guarantee you'll ever see a dime, especially if they don't have significant assets to go after. This is exactly why we believe having enough UIM coverage is just as crucial as carrying good liability limits.

We consider Underinsured Motorist coverage a non-negotiable part of a responsible insurance plan. It's the policy that protects you from someone else's mistake.

How Much Liability Coverage Should I Actually Carry in Colorado?

While the state of Colorado only legally requires you to carry $25,000/$50,000, relying on that minimum is a massive financial gamble. A single serious injury can blow past those limits in the blink of an eye, leaving your personal assets exposed. At Conduit Law, we strongly advise our clients to carry much higher limits.

For most drivers, a good starting point is $100,000 per person and $300,000 per accident (100/300).

If you have more to protect—like a home, significant savings, or a higher income—you should be seriously considering limits of $250,000/$500,000 or even adding an umbrella policy for another layer of security. The small bump in your premium buys you an enormous amount of financial protection and peace of mind.

This blog post is for informational purposes only and does not constitute legal advice. Every personal injury case is unique, and past results do not guarantee future outcomes. Contact Conduit Law for a free consultation.

Get a free case evaluation from Denver's experienced personal injury attorneys. Call Conduit Law at (720) 432-7032 or get a free case evaluation from Denver's experienced personal injury attorneys online.

Written by

Conduit Law

Personal injury attorney at Conduit Law, dedicated to helping Colorado accident victims get the compensation they deserve.

Learn more about our team